For first-half 2017, deposition equipment maker Aixtron SE of Herzogenrath, near Aachen, Germany has reported revenue of €114.1m, more than doubling from first-half 2016’s €55.5m.

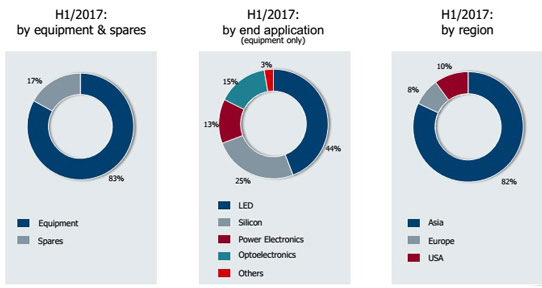

Specifically, equipment sales of €94.4m comprised 83% of total revenue (up from 66%, or €36.6m, in first-half 2016). Sales of spare parts and services comprised the remaining €19.7m or 17% of total revenue.

On a regional basis, 82% of revenue came from Asia (continuing to rebound, after dipping to just 55% in first-half 2016), 8% came from Europe, and 10% came from the USA.

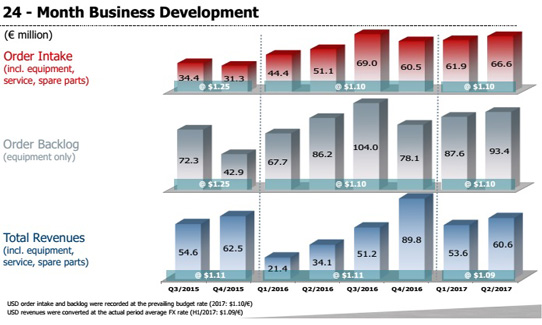

For second-quarter 2017, revenue was €60.6m, up 13% on €53.6m last quarter and up 78% on €34.1m a year ago. Equipment sales of €50.9m comprised 84% of total revenue (up from 81% or €43.5m in Q1 and 72% or just €24.7m a year ago).

First-half 2017 revenue growth was driven mainly by improved demand for metal-organic chemical vapor deposition (MOCVD) systems for manufacturing vertical-cavity surface-emitting lasers (VCSELs), red-orange-yellow (ROY) and specialty LEDs as well as power electronics, and chemical vapor deposition (CVD) systems for manufacturing flash memory.

Gross margin has improved from 18% in first-half 2016 to 25% in first-half 2017, or 27% after adjusting for restructuring costs of €2.3m (with Q2’s 26% down slightly from Q1’s 27%, impacted as expected by low-margin shipments from inventory of the remaining AIX R6 MOCVD systems for GaN LEDs).

Operating expenses rose from €35.9m in first-half 2016 to €40.2m in first-half 2017 (while being cut from €20.6m in Q1 to €19.6m in Q2).

Earnings before interest, tax, depreciation and amortization (EBITDA) have improved from ‑€20m in first-half 2016 to -€10.2 in second-half 2017, or -€4m after adjusting for €6.2m of restructuring costs (improving from -€2.7m in Q1 to -€1.3m in Q2).

The net result improved from -€26.6m in first-half 2016 to €24.9m in second-half 2017, or -€10.4m after adjusting for €14.5m of restructuring costs.

Operating cash flow has improved from -€39.3m in first-half 2016 to €43.3m in first-half 2017, while capital expenditure (CapEx) for property, plant & equipment has been halved from €5.9m to just €3m. Free cash flow has hence improved by €81.3m from -€41m to €40.3m (€33.3m in Q1 and €7m in Q2), due mainly to the collection of receivables as well as advanced payments received from customers.

Cash and cash equivalents at the end of June were €197.1m, up from €193.6m at the end of March but up by €37m from €160.1m at the end of December.

Total order intake (including spares and service) has risen by 34% from first-half 2016’s €95.5m to €128.5m in first-half 2017 (with Q2’s €66.6m up 8% on Q1’s €61.9m and up 30% on €51.1m a year ago, driven mainly by increased demand from LED and optoelectronic as well as memory applications).

Equipment order backlog at the end of June was €93.4m, up 7% on €87.6m at the end of March. Most of the backlog is due for shipment in 2017.

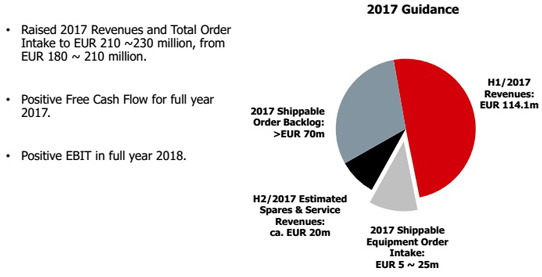

“In H1/2017, the positive development in order intake has continued and will result in improved revenues,” notes CEO Kim Schindelhauer. Aixtron has therefore raised its full-year 2017 guidance for both order intake and revenue from €180-210m to €210-230m (consisting of H1/2017’s revenue of €114.1m supplemented by 2017-shippable order backlog of at least €70m joined by a forecasted €5-25m of further 2017-shippable equipment order intake, plus a forecasted €20m of spares & service revenue).

In addition, in first-half 2017 Aixtron stepped forward in focusing on its core business:

1. in Q1/2017 Aixtron froze product development activities for III-V on silicon (TFOS) materials for next-generation logic chips (resulting in a one-time write down of €6.6m) and in Q2/2017 the firm froze thin-film encapsulation (TFE) activities (involving write downs of €6.4m).

2. as it continues to transform the company to align R&D expenses with revenue (targeting a return to profitability in 2018), on 25 May Aixtron agreed to sell the assets of its ALD & CVD memory product line (based mainly at US subsidiary Aixtron Inc in Sunnyvale, CA) to Eugene Technologies Inc, a US subsidiary of South Korea-based Eugene Technology Co Ltd that makes single-wafer ALD, CVD and plasma deposition and surface treatment systems.

3. To support the ongoing establishment of a joint venture to spin-off its organic light-emitting diode (OLED) deposition technology, Aixtron has founded the subsidiary APEVA SE (with all related staff transferring to the new JV by 1 October).

Dr Felix Grawert will join Aixtron as member of the executive board by 14 August, which means that in first-half 2017 Aixtron completed the majority of tasks concerning the firm’s realignment.

Aixtron says that it continues to transform the firm to align R&D expenses with revenues in order to return to profitability in 2018. As the execution of this strategy may have a substantial influence on profit, management is not guiding on EBITDA, EBIT and net result for full-year 2017. Nevertheless, Aixtron expects to achieve positive free cash flow in 2017 and a positive EBIT for 2018.